If you can look out of your kitchen window and see a grain silo or a wilderness preserve stretching off into the distance chances are good you’re one of the approximately 46 million Americans living in rural communities in the United States according to the most recent U.S. Census data (2010) and data available from the most recent American Community Survey (ACS, 2012-2016).[0]

As a rural American, there is a higher likelihood that you or your neighbors face greater challenges accessing healthcare than those living in urban or suburban communities.[1]

The primary reasons that a person may be unable to access healthcare services include:

- Geographic distance

- Lack of public transportation

- Inability to take time off work (no vacation time or personal days)

- Difficulty communicating (e.g., if English isn’t your first language)

- Cost – including lack of health insurance[2]

And while anyone in the U.S. could experience any number of these challenges, we’re going to look at how rural residents may be especially impacted by some of them, what effect that could have on their health, and some health insurance options that may be able to help.

Reduced Healthcare Access May Result in Poorer Health Outcomes

The inability to access health services can have a negative impact on your health. In fact, not having a primary care physician and skipping routine medical care increases a person’s risk for serious health conditions.[3]

According to the American Hospital Association’s 2019 Rural Report, “The availability of local, timely access to care saves lives and reduces the added expense, lost work hours and inconvenience of traveling to facilities farther away.”[4]

Regular and reliable access to healthcare services can:

- Prevent disease and disability

- Detect and treat illnesses or other health conditions

- Increase quality of life

- Reduce the likelihood of premature death

- Increase life expectancy[5]

That’s why it’s important to understand the challenges and identify options for anyone having trouble accessing healthcare for any reason, including rural Americans.

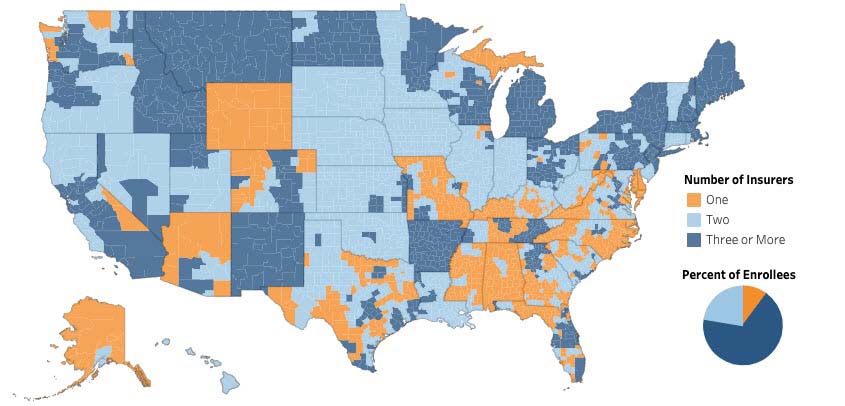

Comparing metro and rural communities’ demographics and health resources: Rural families already have fewer provider options and rural hospitals have been closing at increasing rates over the last five years. From 2015 through 2019, 71 hospitals closed (averaging 14.2 per year). By comparison, from 2010 through 2014, only 47 rural hospitals closed (or 9.4 per year).[9] Why are rural hospitals closing at increasing rates? A few of the reasons include: When rural hospitals close or convert their services (e.g., from a full-service acute care facility to an urgent care), it results in either the elimination of specific services like obstetrics or inpatient care, or elimination of all local access to care.[11] In all cases, affected residents must seek other options – and that can mean traveling longer distances.[12] People in rural areas travel further to access healthcare than those in suburban or urban areas, on average about 10.5 miles total (2018).[13] And rural residents living the furthest from a hospital could drive 34 minutes or more to reach the nearest facility.[14] Proximity to Nearest Hospital (2018)[15] One potential option that may help if your nearest healthcare facility is far away is telehealth. Essentially, if a person is able to make a phone call, or better yet, access a video chat either on their cell phone or computer, they can be seen by a healthcare professional and get help for a variety of conditions. Being able to get a diagnosis and treatment plan for routine or recurring health concerns from home is particularly beneficial when the risks of spreading or contracting an infectious disease are high. Of course, because there is no hands-on exam there are limitations on what conditions telemedicine services can be used to diagnose or treat. Telemedicine plans are not health insurance, but they can be a convenient and relatively affordable way to access a provider 365 days a year from just about any location in the U.S. Learn more about how telemedicine works, including the pros and cons. In the last section, we addressed the challenge of not having a hospital nearby. That issue may be compounded by the prevalence of narrow network health plans. While it can be inconvenient when your nearest hospital isn’t in-network while living in a city, it can be a major obstacle to care for a rural resident. Let’s take a look at this issue next. Compared to urban Americans, rural residents are somewhat less likely to have health insurance, and when they do, they rely disproportionately on public insurance (Medicare, Medicaid, and CHIP).[16] Medicare, Medicaid, and individual ACA Marketplace plans may have narrow networks that can make it challenging to find both affordable coverage and accessible, in-network healthcare providers and hospitals. ACA health plans often include narrow networks as a way to try to keep premium costs lower. In 2019, more restrictive EPO and HMO network plans comprised 72% of all Marketplace health plans.[17] Medicaid insurers tend to have narrower networks as they prefer to contract with providers willing to accept lower payment rates.[18] And it’s actually difficult to know how provider networks may impact access when it comes to traditional Medicare and Medicare Advantage plans. Medicare Advantage (the traditional Medicare alternative offered by private insurers) may have networks as narrow as 46% coverage or as broad as 70% coverage.[19] However, since there is no reliable way to compare plan networks (plan directories are notoriously error-prone), it could be easy to stumble into a narrow network Medicare plan without knowing it. The result for rural residents could be traveling long distances, sometimes exceeding 100 miles, to see a participating physician.[20] Some health plans don’t have network provider limitations. Short term health insurance and hospital indemnity insurance are two types of coverage that may have unrestricted network plans available. These health coverages are not ACA-qualifying. They are considered less comprehensive than ACA plans, are not guaranteed issue, don’t cover pre existing conditions, and aren’t required to cover the essential health benefits. If you’re considering going without health insurance because you’re unable to find an ACA plan with in-network providers, you may want to instead consider one of these options, especially if you can locate one without network restrictions. You can typically apply for these plans throughout the year, not just during the annual open enrollment period. Compare hospital indemnity plans and rates now. Get a Hospital Indemnity Quote Short term policies may provide benefits for services besides just hospitalization, but are primarily designed to help with the unexpected and sometimes higher costs of an accidental injury or illness. Plans can last as little as 30 days or up to 364 depending on your state and the insurer. They also tend to be customizable – you can pay a higher premium for additional coverage or a higher benefits level. Like other non-qualifying coverage, it’s important to read the details of any plans you’re considering since there are more limitations and exclusions associated with temporary health plans, and they aren’t available in all states. See short term health plans available in your area and compare costs. Get a Short Term Medical Quote Besides narrow networks, another challenge for those seeking ACA coverage is the prevalence of high deductible health plans (HDHPs), and for rural residents in particular, having fewer options when it comes to insurers. Rural residents face a trifecta of challenges when it comes to obtaining affordable individual health insurance from the ACA Marketplace: In recent years, high deductible health plans have become more common in rural areas. That means plans with $3,000 to $10,000 annual deductibles. And rural residents have less choice of insurers when it’s time to enroll.[22] In 2020, approximately 10% of ACA enrollees residing in 25% of counties in the U.S. have access to only one insurer offering plans in their area. Many of these counties are rural and/or in the southeastern U.S.[23] And when health insurance is more difficult to obtain, so is healthcare.[24] Insurer Participation on ACA Marketplaces (2020) Let’s look at a couple of options that may help with the challenge of high deductible health plans and lower cost ACA coverage. If you have an ACA-qualifying major medical health plan with a high deductible, a supplemental medical gap plan may help by providing additional benefits for covered injuries or illnesses. Typically, you can use this benefit however you wish. You can apply it to your other policy’s out-of-pocket costs or use it for other expenses like housing, transportation or childcare. Premiums tend to be relatively affordable and are based on a number of factors, including the benefit level you select. Request a quote to find out how much gap plans cost and compare options. Any of these ACA-qualifying options include essential health benefits and pre existing conditions coverage, so may be an affordable option if you qualify. However, it’s still important to validate whether or not nearby hospitals or healthcare providers are in-network since obtaining services from out-of-network providers will increase your out-of-pocket costs. Medicare may be available to you if you’re over 65 years old. Learn more about Medicare eligibility and getting started. Medicaid and CHIP are government-provided coverage options available for low-income individuals, children, and pregnant women year-round. Subsidized ACA health insurance may be available to you at reduced cost via premium tax credits to help lower your monthly premium and/or cost-sharing reductions to help lower your out-of-pocket costs when you receive care. However, these plans are only available during the annual open enrollment period or if you qualify for a special enrollment period. Find out if you qualify for Medicaid, CHIP, or a subsidized ACA plan at Healthcare.gov (income eligibility only). Rural residents may experience greater challenges to access healthcare services, including lack of health insurance.[25] Getting a health insurance plan that you can actually use (affordable deductible, accessible provider networks) may help improve your access to healthcare which could have a positive effect on your health.[26] If you have a high-deductible health plan a medical gap insurance policy may help. If you live a long distance from your nearest provider, a telemedicine plan (not insurance) may help. If you have trouble finding affordable health coverage, look into Medicare, Medicaid, CHIP, or a subsidized ACA health plan. If you have a narrow network health plan or are unable to get an ACA plan that includes your nearest hospital, a non-qualifying hospital indemnity plan or short term health plan may be better options than going without coverage at all. Figuring out your best insurance option can be difficult, especially if you have only a few plans to choose from or one hospital nearby. If you’d like additional help sorting it all out, call [phone_number] to speak with a health insurance agent.

Rural Hospitals Closing

Distance to Provider (miles)

Time to Provider (minutes)

Percent of American Population Affected

Rural

10.5

17

18%

Suburban

5.6

12

24%

Urban

4.4

10

58%

Telehealth Services

Narrow Networks on the ACA Exchange, Public Plans

Health Insurance Without Network Provider Limitations

Less Health Insurance Choice, HDHPs, Lower Incomes

Supplemental Medical Gap Insurance for HDHPs

Qualifying Coverage for Low-Income Individuals and Families

Summary + Next Steps